For self-employed, companies, partnerships, and groups Over 500 covered practices, including healing practices, coaching, management, training, beauty procedures and many more Choice of cover levels - up to £5 million limit available Extensive cover – can include work overseas From application to protection, in minutes Mid-term changes easy Optional extras: cyber liability, workplace contents, personal accident, portable business equipmentand employer’s liability

For self-employed, companies, partnerships, and groups Over 500 covered practices, including healing practices, coaching, management, training, beauty procedures and many more Choice of cover levels - up to £5 million limit available Extensive cover – can include work overseas From application to protection, in minutes Mid-term changes easy Optional extras: cyber liability, workplace contents, personal accident, portable business equipmentand employer’s liabilityWe know understanding the ins and outs of insurance can be confusing, so here we want to keep things simple.

So, being specialists in the insurance market with over 14 years of experience, we designed this combined product to fit the needs of freelancers, businesses and groups. It could indemnify you up to your chosen cover level for different situations that can occur during the course of your work. Whether it’s a customer hurting themselves at your premises, you doing something you shouldn’t have, or one of the products you use in your practice causing damage, these are all mishaps that occasionally happen and could lead to a devastating claim against you.

Having our combined professional indemnity, public liability and medical malpractice insurance provides you with total peace of mind – knowing that in the event of a claim, someone else will take up your battle. If it’s found that you (or one of your employees) did do something wrong, the insurance will cover the legal and compensation costs up to the level you chose – meaning you and your business are safe.

If you provide a service of any kind, even if you do so free of charge, regard it as a hobby or make only a small income from it, there is always the possibility of someone making a claim against you – that you did something wrong, or perhaps didn’t do something that you should have done.

With the best will in the world, even the most honest and professional person can make a mistake. Worse, allegations can be received and have to be fought evenif you are blameless but have to prove it!

Should this happen the consequences can be drastic: not only can it be very stressful and time consuming, but legal costs escalate fast and if the claim is successful the compensation to be paid can cripple your business. Of course, if you’re a sole trader your business is ‘you’, in which case it will be your personal assets (savings/ property equity etc) that will be used to cover the costs.

So, the question is, 'Would you want help handling such an unfortunate situation, and with cover costing so little, doesn't it make sense to have it?'

Note: on this page you will find abbreviated information for guidance only – subject always to the full Policy Wording.

As this is a policy ‘in aggregate’, all of the listed liabilities below would be covered up to your chosen cover level, which means that one or more claims can be covered by this policy, as long as its requirements are met and the whole amount does not exceed your chosen cover limit.

This policy is written on a claims made basis which means that the policy covers you for claims made against you and notified to us during the period of insurance. An exception would be if you received a claim during the period of insurance for something you did before obtaining thing insurance, if the event occurrence falls within the period of your retroactive date.

The cost of your policy will vary depending on a number of factors (see below), but here is an example of a typical policy:-

£1 million indemnity cover for 1-2 people in a business with a turnover of up to £125,000 per year, that does not work with overseas customers.

Only £122.64 ( or £10.80 per month ) or from as little as £98.04 ( £8.60 per month ) if you are from one of our recognised organisations

Always give accurate information when applying for insurance. Any misrepresentation could invalidate your policy.

The cost of your insurance will vary depending on the following:

The number of people to be covered.

You should only include those people employed by you, or working on your behalf under your business name, who provide the service for which you are seeking insurance. People who perform a purely administrative role do not have to be included.

The level of indemnity cover required.

You can choose from £1,000,000, £2,000,000or £5,000,000. For many people £1,000,000 is sufficient but if you use public venues you will often find that they will require you to have £5,000,000.

The size of your business.

In this particular situation size is determined by the turnover of your business. This is how much income your business receives in a year – NOT the profit you are left with after expenses, or the amount you pay yourself.

You don’t have to worry about knowing the exact amount but will be asked 'to choose from our range of income brackets, the lowest of which is up to £125,000'.

Whether or not you do business overseas.

You must inform us if you conduct business with overseas clients. If this includes the US and Canada it will increase your premium.

Discount

Westminster is very pleased that many training organisations, accreditation bodies and membership groups recommend our insurance to their students or members, and in turn we support the professionalism that these organisations encourage by offering a discount to their students/members.

If you belong to such a body then please ask them or us if they are one of our recognised organisations.

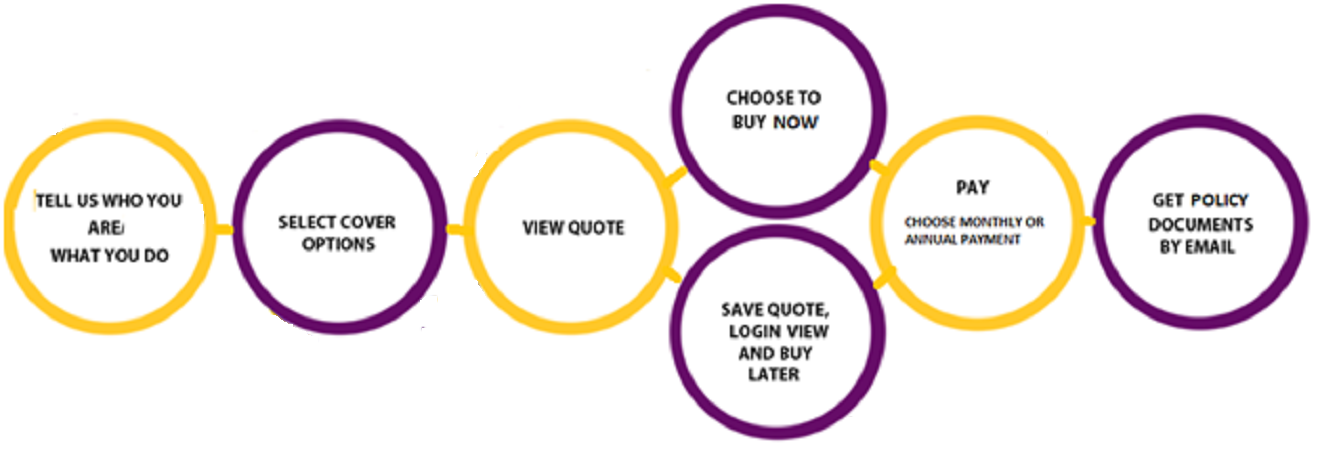

Getting a quote, or multiple quotes, and buying insurance from Westminster couldn’t be quicker or easier. You can have your documents in minutes. All online, you can do it whenever suits you best and be in control of the whole process, but if you have any questions we are more than happy to hear from you.

Our policy is 'Claims made' and covers Professional Indemnity, Public Liability, and Medical Malpractice Insurance under one simple policy. But what does that mean when it comes to claims?

Here’s an example:

You run a sports and health coaching business and have £1,000,000 in cover.

That’s £150,000 in claims—plus legal fees and reputation management costs

Since your policy covers all three types of insurance, and you report the claims promptly, we cover the costs up to your chosen limit.

In short: If a claim arises during your policy term and meets the policy criteria, we’ve got you covered—legal costs included.

The Law and Jurisdiction of the policy is specified as ‘The Law of England and Wales’. Law and jurisdiction are two different matters. 'Law states what country's laws are to apply to the contract, and the 'Jurisdiction' is which country's courts are to have jurisdiction. Both are in relation to disputes arising out of the contract between the Insurer and the Policyholder.

The Territorial Limits are the countries and territories where the policy will provide cover to the Policyholder. This is where the policy will accept the serving of formal legal action against the Policyholder. The insurers will respond to a valid claim from a country or territory within the Territorial Limits of the policy, and the courts of the country from which the claim arises shall have the jurisdiction to hear the dispute arising out of the contract.

Public Liability Insurance protects you if someone claims your business caused them injury or property damage. This applies to any member of the public, not just clients.

It covers incidents not directly related to your professional work but that still happen due to your business activities.

Example Scenario:

A visitor walks into your office, trips over an item left on the floor, and suffers a nasty head injury - easily done, isn't it? They could claim for medical costs and compensation which easily amount to thousands of pounts. Public Liability Insurance covers these types of claims, helping protect you from financial loss.

In short, it’s a safety net for unexpected accidents involving third parties.

We all make mistakes—or sometimes, clients think we have, even when we haven’t. Could your business handle the financial impact of a legal claim?

Example Scenario:

During a coaching session, you give advice that a client later claims was misleading or harmful. Perhaps they left their job and haven't been able to secure a new one - they blame you. They make a claim against your business for financial compensation to cover their loss of income and the mental distress it caused.

Of course, you may have done nothing wrong, but even so, you have to pay legal fees to defend your position - this and potential payouts can be crippling.

How Professional Indemnity Insurance Protects You

Also known as Malpractice Insurance, this cover protects you against valid Claims that arise from you practicing your professional service. It ensures you won’t have to pay out of pocket if a client makes a Claim over something you did—or didn’t do.

For any professional offering advice, expertise, or services, this insurance is a must-have safety net.

Yes! Public Liability covers physical damage, while Professional Indemnity protects against negligence claims - that you did something you shouldn't have done, or that you didn't do something you should have done. Our policy includes both Public Liability and Professional Indemntity so you are fully covered.

Our policy is a Claims Made policy.

This combined with a Nil Retroactive Date means that your insurance will cover Claims that you first become aware of and report during your policy period, even if the incident happened long before, provided that when you purchased the insurance you had no reason to believe that there were any past events that might lead to a Claim. If you think there might be, you must disclose this during the quote application.

The key dates that matter are:

If your policy has no retroactive date (shown as 'Nil') you are protected for past work as long as you keep renewing the policy. However, if you stop working, you’ll need ‘run-off’ cover, which keeps you protected against future Caims related to past work.

A Claims Arising policy works differently. It only covers Claims that occurred during the active policy period, meaning the insurer who covered you at that time will handle the Claim—no matter how many years later it’s reported.

Important: If you ever switch from a Claims Made policy to a Claims Arising policy, you could end up losing past coverage if you’re not careful. Always check before making any changes to ensure you stay protected.

No, you are not covered if you work outside the insured group.

Here’s why:

This insurance only covers the policyholder, which in this case, is the group. If a claim is made, it must be against the party responsible for the service provided.

If the group was responsible for the service, the insurance may cover the claim—including work done by individuals on behalf of the group.

However, if you personally provided a service outside of the group (even if you are a member), you are not covered. The claim would be made against you as an individual, not the group’s insurance policy.

In short: If the group is insured, the group is covered. If you work outside of it, you are not.

It depends on what you actually do at the pamper party.

If you are providing treatments, therapies, or services that are already covered under your policy, then yes, you’re covered—at no extra cost.

However, it’s important to check the specific descriptions of the services covered in your policy. If what you offer at the pamper party falls outside of those, you may need additional coverage.

Before hosting group sessions, review your policy details to ensure everything you do is included. If you're unsure, feel free to contact us for guidance.

Yes, your business can still be covered, even if employees or directors live abroad.

However, what truly matters is where the business operates and where any claim is made—not where individuals reside.

Our policy covers the policyholder (whether that’s an individual, company, or group) for claims made for services provided within the Territorial Limits, and will be subject to UK jurisdiction. This means:

So, while, for example a director living in Singapore (or any other country) does not affect the policy, it does not mean claims from anywhere in the world will be accepted. Only claims falling under UK jurisdiction will be considered.

Our policy is what is termed a ‘Claims made policy’. That means the insurers will consider a claim that they are advised of (and you must tell them at once!) during the policy year. The incident that caused the claim could have occurred in the recent past – and it could have been years before, provided the incident occurred AFTER the retroactive date. Our policy has no retroactive date and therefore our policy covers you during the policy term for an incident that could have occurred at any time in the past, provided that, at the inception of the policy you were not aware there was a possibility that the incident could lead to a claim.

Out of hours messaging service if you need us urgently

Copyright ©2026 Westminster Insurance Ltd Authorised and regulated by the Financial Conduct Authority for regulated business conducted in UK FRN: 439023.

Specialist in fully automated on-line insurance delivery to customers in UK, USA and Canada. Your resource partner to deliver high quality, cost efficient, fully automated insurance direct to the customer by Internet anywhere in the world, on your behalf.

Comprehensive - Competitive - Convienient